I have waited quite some time to share this story with you. To be honest, I was afraid to be just another money blogger shouting, “look, I paid off my debt!”

But we’ve been around for a couple of years now (as of this week!), and enough people have asked me about this story that I finally realized something. I realized it’s not a story about me or my family or what we’ve accomplished. It’s about you.

It’s about the money struggles we all face. The ones that seem completely insurmountable. The ones that make us feel overwhelmed and isolated from the people we love.

Maybe your challenge is a massive pile of school debt like mine was. Perhaps it’s an underwater mortgage, a retirement plan that looks more like an “if” than a “when,” or simply keeping the bills paid when your income isn’t keeping up.

We all have some big, scary dragon to face in our financial lives. I want to tell you about one of mine to remind you that you’re not alone. And most importantly, I want to show you that with a drop of strategy and a gallon of gall, you can slay anything.

Life and Debt: My Story

I remember joking with a friend toward the end of college about how I had just recently calculated my net worth for the first time. I was pleased to report that it was over six figures, but I was less pleased about the minus sign in front of it.

Most adults living in the 21st century will be dramatically unsurprised by my descent into debt.

It is tragically normal.

The Way Down

If you read my recent (somewhat sassy) story of how I paid for college by working a summer job, you’ll know that I did not, in fact, pay for college by working a summer job. (To clarify, I did have the summer job, it just didn’t pay for college, like, AT ALL.)

At 17, I joined a private university with no savings and no real plan. I worked through high school and college but barely made a dent in my tuition. Even with a big chunk covered by scholarships and grants, I still racked up tens of thousands of dollars in debt each year.

Midway through my last year of school, I accepted a cushy corporate job offer. I was sure that all my money problems were now solved (ha). So I immediately put my signing bonus down on a $20,000 loan for a car. Because why not.

Later that year, I proposed to my then-girlfriend, and she said yes. So we packed up our dog and the few things we owned into our new $20k liability and headed across the country to start our new life.

Soon after, we merged finances — one small Roth IRA, some savings bonds, a few scraps of cash in a bank account, and two massive piles of debt.

The True Cost of Debt

We got set up in our new home city, started working our fancy new jobs, and quickly realized that something wasn’t working. As we began to manage household finances for the first time, we finally started seeing our debt for what it was: an absolute monster.

In total, we had 26 outstanding loans:

- 19 federal student loans (mostly mine), Total: $66,762.77

- 6 private student loans (all mine), Total: $80,962.00

- 1 car loan (also technically mine, though we did share the car), Total: $19,381.52

- Grand Total: $167,106.29

The combined minimum payments on all our debts (the minimums, mind you) made up nearly $2,000 every month. That was more than our already-expensive rent. Equivalent to a modest international vacation every month. Almost $25,000 a year that we could have been saving for our future.

We were making more money than we ever had, yet feeling further and further behind every month. Something needed to change.

Enter the Debt Dragon

We started learning everything we could about money and debt. Finally, we landed on a basic strategy for how we would get out. We would just need to stick to it consistently for a few years. But there was still one thing missing. We needed a clear motivator to keep us on track when we started to lose steam.

We needed a reminder of what we were fighting for (and against).

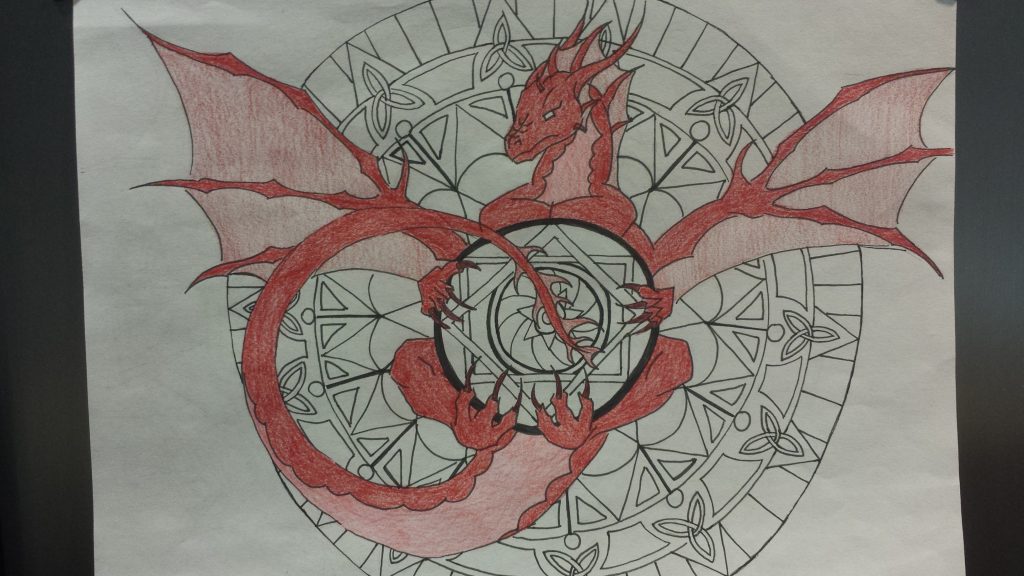

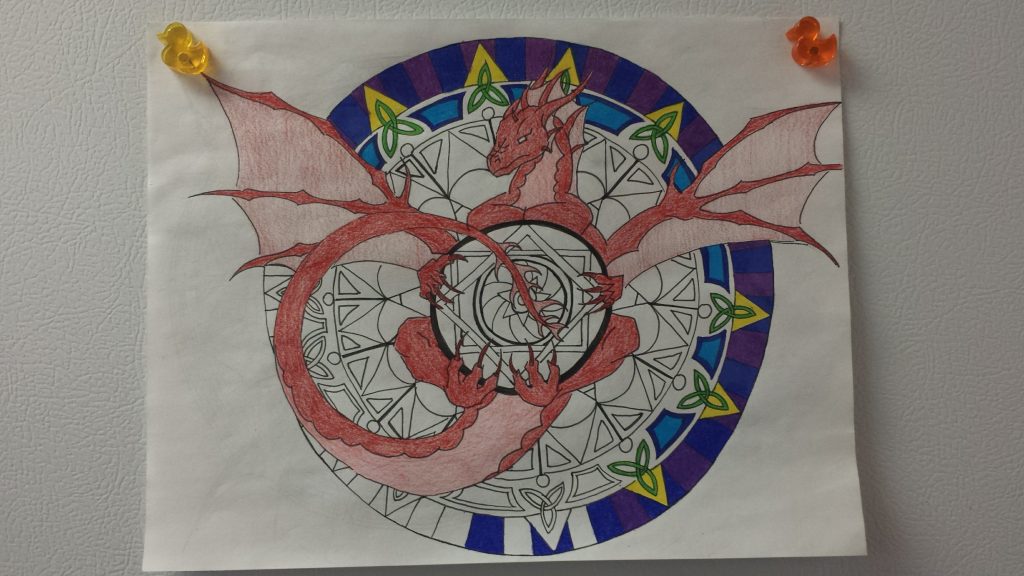

So we (by which I mean she alone) made a drawing. It was a mandala — a complex pattern full of little shapes — based on a similar one we had found online. This particular mandala was ensnared by a dragon.

Initially, we only colored in the dragon itself. We intentionally left the rest of the design empty. Then, we would color in a cell of the drawing every time we paid off a certain amount of the debt (we decided on $800 as our number).

The plan was to keep the drawing always visible in our apartment. A reminder of what we were working toward and how much progress we had made so far.

And most importantly, it gave our struggle a name. We now knew the face of the monster we needed to defeat: our very own debt dragon.

The Way Out

Slaying a dragon is no small thing. But neither is the treasure it guards. So once we had our quest laid out before us, we got straight to work.

Defeating that dragon, and getting ourselves entirely out of debt, became our sole focus. We were determined to do everything it took to zero out every last penny we owed as quickly as possible.

At first, we hoped to be done in about seven years, before we turned 30. Whenever we mentioned this, people told us to be realistic or that “it doesn’t work like that.” However, once we got going and got used to adjusting our habits to fit our plan, we started to think we could get there in five years. Ultimately, we were completely debt-free after just two and a half years.

No more minus sign.

What Worked For Us: 9 Creative Ways to Pay off Debt

As I said at the beginning, we all have our dragons to slay when it comes to money. Yours may be debt, like mine, or any of about a hundred other perilous adventures.

Whatever dragon you face, the best way to defeat it is to face it squarely and throw your whole self into the endeavor. There are no shortcuts to this process, but it also hasn’t failed yet.

What follows is a list of the tactics and mindset shifts that made the most significant impact in helping my family get out of debt. But they’re not just about paying off debt. This framework has helped us succeed with our money many times since.

Whatever dragon you now face, I hope these methods will be of some help to you too.

1. Make a Plan

Any great endeavor you set about without a plan is doomed to fail. This is no less true with a significant money goal than anywhere else.

Now, I’m not saying that everything will go according to that plan, or that you should expect it to do so. But you need to start somewhere and clearly know what you will do next.

With debt, that means focusing on one loan or liability at a time in an order that makes sense to you. Pay the minimum you can on everything else, and put as much money as humanly possible toward eliminating just one source of debt. If you’re unsure what you want that order to be, most people go with either the avalanche or the snowball method.

2. Visualize It

The debt dragon itself — the physical drawing — was a key component for us. A daily reminder of our goal and a tracker of how much progress we had made so far helped us stay motivated.

Bonus — it made great opportunities to open up conversations about debt and money whenever people asked. Honest conversations with people we trust are essential in maintaining our financial wellness. Plus, since it was only a drawing with no numbers or labels attached, we didn’t have to share the exact details of our debt situation with anyone if we didn’t want to.

3. Hit It From All Sides

When you’re facing a personal financial crisis like slaying the debt dragon, you need to hit it with your entire focus and your full power.

When we started paying off our debt, we were fortunate enough to have pretty high salaries from our day jobs. But we didn’t rest there. We didn’t let that hold us back from trying everything we could to raise our income and lower our expenses.

Anything that would free up more cash every month to throw at our goal, we did.

She started multiple side gigs, and I took on extra overtime at my day job. We both tried out driving for rideshare services on the weekends. We cut our expenses mercilessly.

Mind you, was this effort a sustainable one? No way, and it wasn’t meant to be. We did not expect to continue holding down five jobs between us or slashing our spending forever. Why? Well…

4. Make It a Sprint, Not a Marathon

With most types of goals, you tend to be better off with a long-term mindset. When it comes to things like habits and big professional projects, the thing that you can consistently do always beats the thing that you can do intensely for a short while.

But it doesn’t work that way with debt or most other money problems. When you’re paying off loans, you don’t want to build a routine that you’ll be able to keep doing ten years from now because you don’t want to still have this problem ten years from now!

The longer your battle with the debt dragon goes on, the more time it has to regain its strength through interest, fees, and who knows what else. And the more exhausted you become. So fight hard and end this thing swiftly.

5. Consolidate

This one has both a literal meaning and a symbolic one.

Consolidation can be (but isn’t necessarily) a great strategy to help you get out of debt faster. If you have a large number of loans with high interest rates, poor terms, or that are held by an especially predatory bank, it could be worth refinancing to get a single, lower rate. Less interest and fewer fees mean more dollars in your pocket for knocking out the principal!

And metaphorically speaking, consolidation is a great way to think about any financial dragon. Don’t let many faces of a single problem divide and conquer you. Get all the bills, debts, and information you need into one place and hit that problem with 100% focus.

6. Don’t Sacrifice a Single Thing

This is a simple but potent money mindset technique.

Whenever people talk about doing something with their money that will benefit them in the future more than the present, they tend to use words like “sacrifice.”

This keeps the focus on what you’re “giving up.” But often, you don’t miss whatever it is you were “giving up” in the first place. And you definitely will notice what you end up gaining instead.

Treating progress as a sacrifice is one of the most common money-saving mistakes. Likewise, it will only get in the way of you paying off debt. Instead, flip the switch by focusing on what you’re doing for yourself, what you’re giving yourself in place of that short-term want, and you’ll quickly find yourself enjoying the process a lot more.

7. Fall in Love with Saving

Choosing to stop treating your primary money goals as some punishment you have to go through is a great start. But if you want to seriously accelerate your progress toward the place you want to be, the trick is to fall in love with the process.

For instance, almost any big money goal – paying off debt included – involves saving money. The money you save is the fuel for whatever else you want to accomplish. And I get it; saving can be slow and tedious.

But it can also be a thrilling adventure if you let it.

Treat saving like a game. Like a skill you are practicing and honing by the day. For example, instead of being disappointed by not going out to lunch on a particular day, try feeling excited about the $20, $40, or $80 that your choice freed up for what you truly care about: building a future free from financial stress.

8. Leave Nothing on the Table

Most of us have a wealth of financial opportunities sitting well within arm’s reach. Some of these may be small. Others may require a bit of creativity on your part. But when you get serious about getting out of debt, reaching your retirement threshold, or slaying any other money monster, you start to see these possibilities all around you.

For instance, at your job. You already take advantage of your paycheck and (hopefully) any retirement plan available. But what about the weird little stuff like:

- Discounts on products or services

- Lifestyle discounts on health insurance

- Education reimbursements

- Complimentary coffee/snacks (hey, it’s still something!)

Every company is different, but most jobs have at least a few extra things you can take advantage of. For example, I once got a free toaster oven through a healthy habits program at work. Sure, a toaster oven won’t pay off anyone’s loans. But hey, it makes excellent toast. For free.

Individually, none of these things is life-changing. But on a short-term sprint to get out of debt, a few of them together can make a big difference!

And it’s not just at work. Look for deals. Use your gift cards. Try out free products and services when they’re available. Keep your eyes open for anything that can help you move the needle.

9. Windfalls are Power-ups

When you hear the word “windfall,” it sounds like something that only happens to other people, right? Most people associate the term with massive and rare events, like receiving a large inheritance or winning the lottery.

Monetary windfalls are far more common than that, but you may not be thinking of them as such. You may receive a windfall in the form of:

- Annual bonuses at work

- Cash gifts from family and friends

- Tax refunds (technically your money to start with, but still a surplus in the budget)

- $10 from winning second prize in a beauty contest (you’re gorgeous, we all know it)

Any amount of money you receive that is unexpected or outside of your typical monthly income should be considered a windfall.

On receiving a windfall, most people will quickly find a way to spend it – on anything from a night out on the town to new kitchen appliances to a big vacation. But if you’re serious about dramatically changing your financial life, windfalls (small or large) are a great way to pour more fuel on the fire.

Slaying Your Own Debt Dragon

Like I’ve been saying all along, this isn’t my story. Sure, I’m one of the only two (human) characters in it, and I didn’t even give the other one a name. Just “wife,” yeesh.

Okay, it was a little bit about me. But more importantly, it’s about you, your kids, your parents, your neighbors, all of us. We all face these monstrous, intimidating challenges with money at different points in our lives.

I finally decided to share this story to tell you that you can slay your dragons too. What we did wasn’t unique. It was something anyone can do with enough enthusiasm, perseverance, and most of all, focus. Of course, we had some advantages on our side, as well as some disadvantages flying in our faces, just as you no doubt do as well. And we stayed true to our quest all the same.

Try to identify the giant dragon in your financial life right now. Give it a name and a face. Then, as soon as you do, gather up your armor, your sword and shield, your potions and poultices, and let’s slay this thing.

Very specific suggestions, especially creating visual model to monitor progress. Congrats on slaying your dragon.

Thanks, Peg. Very grateful to be where we now are because of this journey. Plus, everything that we learned along the way, I wouldn’t trade for the world!