The Individual Retirement Account, or IRA, rivals its cousin, the 401(k), as one of the most effective ways for an everyday investor to build wealth. However, wading through the sludge of terminology, rules, numbers, and targeted advertising can make it frustrating, dare I say even bamboozling, to navigate the basics of IRAs.

Whether you are considering opening up your first IRA or already have one and would like a better grasp of how it works, it’s not as scary as it may feel. Below, you’ll find everything you need to know about how IRAs work, what makes them so incredibly powerful, and how you can take charge of yours.

What Is an IRA?

At its core, an IRA is an investment account. Like any other investment account you open, it can hold a mix of financial instruments such as stocks, bonds, mutual funds, and more. However, what separates IRAs from common brokerage accounts is the numerous advantages designed to benefit people saving for retirement.

A common analogy is that an IRA works like a jacket or an umbrella. If you take an ordinary investment account and wrap a comfy coat around it that offers various protections and benefits for long-term investors, then you’ve created a retirement account.

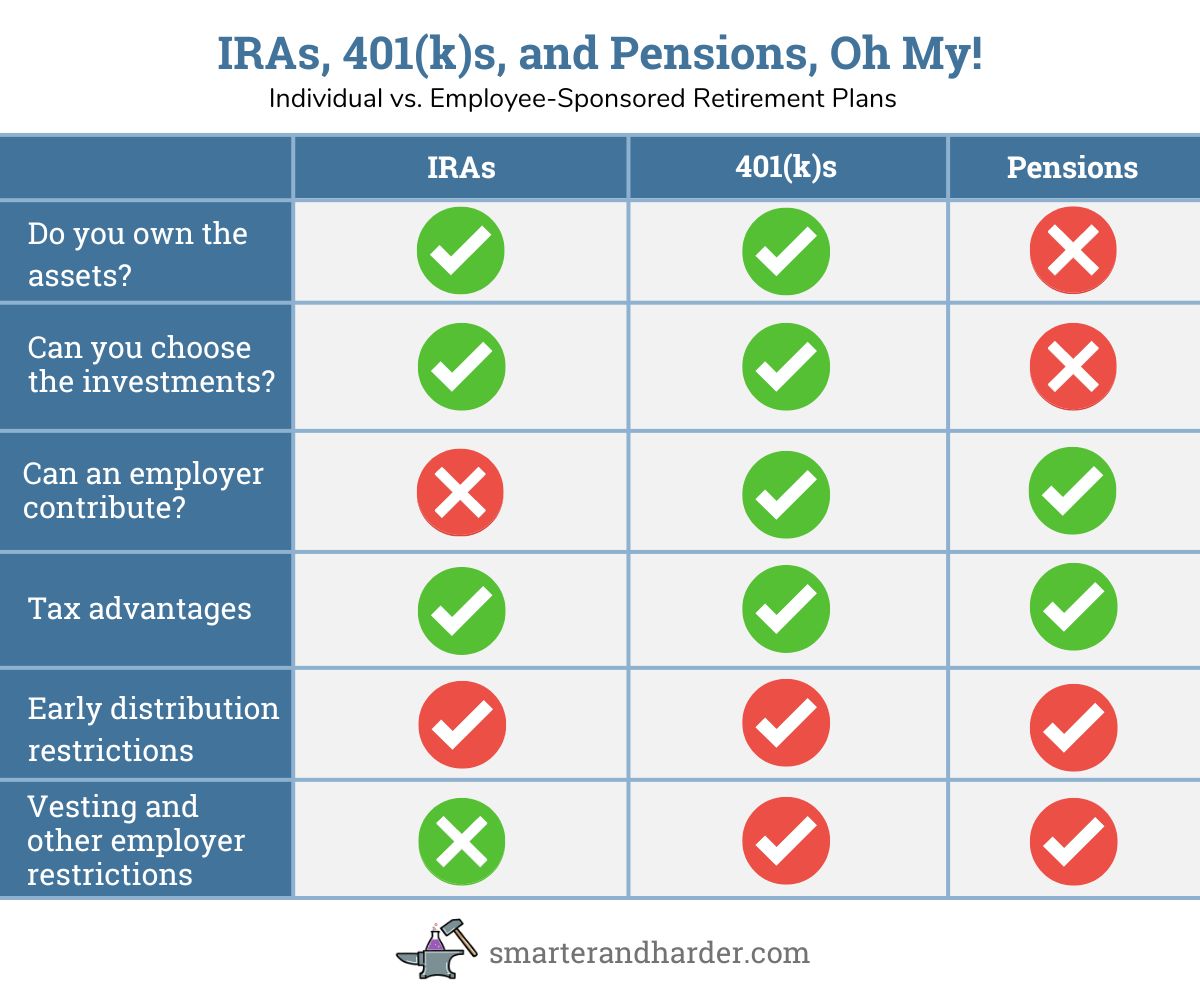

The main thing that distinguishes an IRA from other retirement accounts is that you, the investor, own it outright and are free to manage it at your discretion. An investor typically creates their own IRA rather than an employer offering it with specific parameters such as vesting schedules.

Benefits of an IRA

If you are an ordinary person looking to start saving money for retirement, an IRA is likely the best place to start. Its only competition would be a solid employer-sponsored offering such as a 401(k) with a good match, but even then, there’s some debate.

IRAs offer crucial advantages that can help you build wealth and save for retirement that other accounts simply can’t match.

Tax Advantages

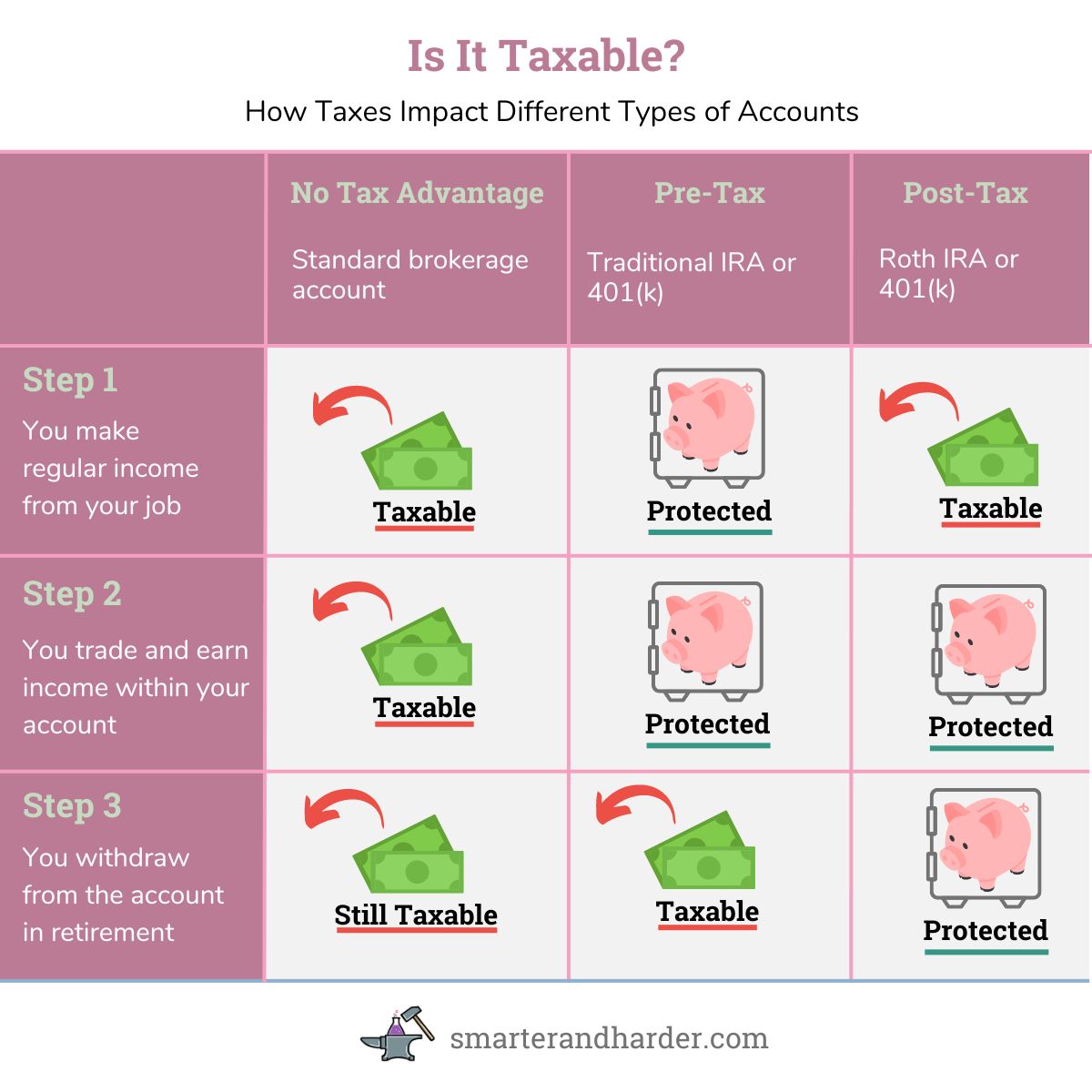

The most crucial benefit of IRAs is taxes. Investing money for your golden years without using a retirement account would typically follow this process:

- Earn money from your job and pay income taxes on it

- Invest some of that income, and pay additional taxes on any trades you make or dividends you earn as the money grows

- Distribute money from your investment accounts during retirement, and pay more taxes

There are multiple types of IRAs, but most can shield you from taxes in at least two of these three stages. Since taxes can severely dampen investment growth over time, this protection is one of the greatest advantages available to everyday investors.

It is technically possible in some cases to sidestep all three of these stages of taxes with IRAs. However, it involves a somewhat complicated loophole and some accounting witchcraft, so we won’t get into it today. If you’re curious, this strategy is called the “Mega Backdoor Roth” IRA.

Ownership and Autonomy

While most retirement accounts offer some tax advantages, the IRA outshines its peers in its first initial: I for Individual. Unlike a 401(k), 403(b), pension, or employer-sponsored annuity, you have complete autonomy over your IRA.

Most employer plans require you to hit specific vesting timelines before you are fully entitled to the money in your name. They will also limit your investment options based on the broker or retirement company your employer uses.

Unlike 401(k)s, pensions have the added disadvantage that you don’t own the assets within them. While your contract may entitle you to payments based on your contribution to a pension fund, you don’t own it. That means you have little or no say in its management, and if it goes bankrupt, you’re out of luck.

With an IRA, you choose the brokerage or institution to hold your account, select the investments you want, and own everything in that account. Besides the basic IRS rules, no one can restrict your access to or ownership of those assets. And crucially, no one can pull the rug out from under you if they go out of business.

Downsides of IRAs

While IRAs are a fantastic option for helping almost anyone save for retirement, they also have a couple of tradeoffs to consider.

First, unlike some employer-sponsored alternatives, most IRAs don’t offer matching opportunities. The primary advantage of 401(k)s and similar plans is that many employers will match some or all of your contributions, accelerating your account’s growth. The tradeoff for an IRA being entirely your own is that no one else has incentive to match your contributions.

Besides the opportunity cost of missed gains on an employer match, IRAs share one obstacle with virtually all retirement accounts. Namely, you cannot withdraw money from your account prior to retirement without paying severe penalties. These accounts are specifically designed for retirement savings, and using the money for other purposes comes at a hefty premium.

Different Types of IRAs

So far, we’ve mainly looked at IRAs as a monolithic retirement vehicle, but there are several distinct types. Each has unique advantages, and some also have specific eligibility requirements.

Traditional IRAs

A Traditional IRA, so-called because it was the original variant, is also sometimes referred to simply as an IRA. It is a pre-tax, or tax-deferred, account.

The money you put into this account is not susceptible to ordinary income tax and will be deductible from your taxable income for that year. However, when you withdraw the money in retirement, that income will be taxable.

Roth IRAs

A Roth IRA, a more recent iteration, is essentially the opposite: a post-tax account. You will pay ordinary income tax on the money you use to fund a Roth; it is not tax deductible. Then, in retirement, your distributions from the account will be tax-free.

Roth IRAs originated in the late 1990s and quickly rose to prominence alongside the Traditional version. The Roth variant has become so popular that it is now also common in other types of accounts, such as Roth 401(k)s.

Unlike Traditional IRAs, there is a limit on who can contribute to a Roth. As a result, high-income households may be ineligible for this option.

Roth vs. Traditional IRAs

Recall the three stages of taxes discussed above — in a non-tax-advantaged scenario, you pay taxes on:

- Your regular job income

- Trades and income within your account

- Distributions from the account in retirement

A Traditional IRA shields you from taxes on the first step, a Roth does so on the third step, and both protect you on the second. Trades and income within an IRA are always non-taxable.

There is much debate over which of these two accounts is ideal, and for whom. One common determiner is your current income level vs. your expected income in retirement.

If you expect your income today to be higher than it will be post-retirement, then you would pay less tax overall in a Traditional pre-tax account. However, if you expect to be in a higher tax bracket in your mid-60s onward than you are now, you would do better to pay your taxes now at the lower rate. The latter scenario favors the Roth, which is the better choice in most cases, especially early on.

Both of these accounts are excellent options. While some folks love to debate the finer points, either type will massively improve your ability to build wealth. So don’t sweat this distinction too much.

SEP and SIMPLE IRAs

There are two additional types of IRAs that will only apply to people in specific situations: SEP IRAs and SIMPLE IRAs. These are mainly for small businesses and self-employed individuals who may not have access to larger, more complex retirement plan offerings.

A Simplified Employee Pension or SEP IRA allows an employer to make retirement contributions on the employee’s behalf. The employee does not contribute directly, but they fully own the account.

A Savings Incentive Match Plan for Employees, or SIMPLE IRA, allows small businesses to set up simple retirement accounts with matching for their employees.

These accounts are effectively hybrids between IRAs and 401(k)s. While their employer matching and separate contribution limits resemble the latter, their 100% employee ownership and lack of vesting schedules remain true to the former.

Who Can Open an IRA?

Fortunately, IRAs are not very exclusive. According to the IRS, almost anyone of any age can open and contribute to a Roth or Traditional IRA. As long as you or a spouse have earned taxable compensation in the given year, you can most likely put some of that income into an IRA.

There are only a few rules about who can contribute and how much:

- People above a certain income level cannot contribute to a Roth IRA. The limit varies by year and filing status but is typically over six figures.

- There is no income limit for Traditional IRAs.

- You can only contribute a limited amount to your IRAs each year. For 2023, this amount is $6,500 across your Roth and Traditional accounts.

- Individuals aged 50 and older can contribute an additional $1,000 per year in “catch-up” contributions. For 2023, that limit would be $7,500 total.

A crucial observation about these rules is that they generally don’t restrict who can contribute. Instead, they limit how much a person can benefit from the tax advantages. These accounts are lucrative enough that the IRS needs to limit their use. To the savvy investor, this should be a strong incentive to max out their IRAs each year.

How to Start Your First IRA (5 Steps)

One of the best things about IRAs is that starting one is relatively straightforward and painless. If you’re considering taking the first step on your retirement saving journey, start with this basic outline for finding and setting up the right account for your situation.

1. Set Money Aside

The first thing you’ll need to start your retirement account is some money to go into it. Unlike with employer-sponsored plans, this will be all you. While that’s a terrific thing in most regards, it also means it’s on you to find and set aside the cash to fuel it.

There is no real minimum for starting an account. You could open yours with $5, or even no money at all. Some institutions or individual investments will have minimum amounts required for you to invest, but the account type itself has no minimum.

If you want to start seeing growth in your account quicker, it’s better to start with at least a few hundred dollars. However, even by opening an empty IRA, you will have taken the critical first step toward achieving your retirement goals.

2. Decide What You Want

Once you know how much money you’re planning to start the account with, the next step is to figure out a high-level plan.

Do you want to open a Roth IRA or a Traditional? If you’re unsure or don’t want to think about it too much, start with a Roth.

Which institution will you use for your account? Vanguard is an excellent option with low fees, great support, and a wide variety of investment choices, but Fidelity and Schwab are also popular options. Many also turn to robo-advisors like Betterment and Wealthfront for their modern approach to low-cost retirement account management and advising.

Finally, you may want to start thinking about the investments you want in your account, but you don’t need to have that entirely figured out yet.

3. Create The Account

This step may sound the most intimidating, but it’s actually the simplest.

Once you know which type of IRA you want to start and where you want to start it, head over to their website and start creating your account! They will ask you a few personal and financial questions, and you could be up and running in as little as a few minutes. And that’s it!

Part of this sign-up process will likely give you the option to pull in the money you set aside in step 1. If not, there should be an easy option once you log into your account.

4. Choose Your Investments

If you made it to this step, congratulations, you have a retirement account!

Once you have money inside your IRA, it’s time for what will probably be the most challenging part of the process: deciding how you want to invest it.

If this retirement account is your first experience with investing, as it is for most people, start by taking a long, deep breath. You can do this.

You will encounter a seemingly infinite pool of options and at least twice as many opinions about them. There will be complicated terms and piles of numbers that don’t really matter.

For almost everyone, building a simple, straightforward investment portfolio is all you need to steadily and reliably amass wealth over time. Start simple, and go from there.

5. Make a Contribution Plan

Almost all of the hard work is out of the way, but there is still one step that is absolutely vital to the process.

Once you have started an IRA and allocated it to a few basic investments, you have constructed an indomitable wealth-building machine that can transform your life. However, that machine needs fuel. The more money you can save and contribute to that machine, the more beautifully and powerfully it will run.

The money you contribute to a retirement account will grow — slowly at first and then, over time, at a pace that’s hard to imagine. Anything you can safely add to this snowball effect will multiply itself over the years. Reaching the annual $6,500 contribution limit is a terrific goal, but even $10 a month is way more than nothing.

The most effective way to save for retirement is to determine what you can safely set aside each month or year, then automate that contribution so you’ll be building wealth on autopilot. Most brokers offer a straightforward way to do this.

One last thing to keep in mind at this stage — this money will effectively be inaccessible until you reach retirement age, so be careful not to overextend with savings you might need sooner. Other than that, you’re all set to go!

Cruising to Retirement With an IRA

IRAs are such a powerful tool for building wealth and saving for retirement that the government limits how much we can use them. If that’s not a sign there’s something incredibly valuable here, then it’s hard to say what is.

For many people, a retirement account is their first experience wading into the world of investing. When that’s the case, it can feel like an overwhelming circus of information, charts, and jargon. However, when it comes down to it, the basics of IRAs are something anyone can use to take charge of their retirement and radically change their financial future.