Today it is possible, sometimes even required, to buy insurance for everything from homes to video games and from medical bills to wedding dresses.

With such a deluge of options, how do we take suitable precautions without wasting time and money on cash-grab insurance schemes? The answer, at least in part, lies in knowing when we need to forgo traditional insurance plans and establish self-insurance.

The Core Purpose of Insurance

To make informed decisions about insurance, when to pay for it, and how much to pay, we first need to take a step back. We need to remind ourselves what insurance is for in the first place to understand best when we do and don’t need it.

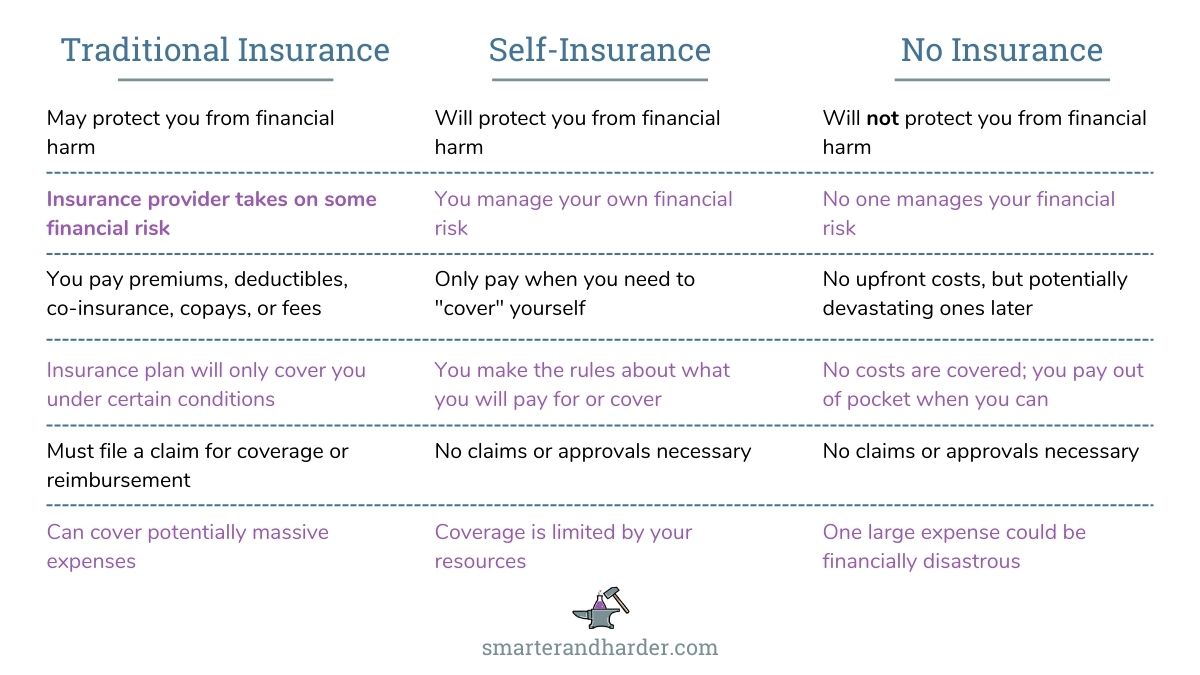

At its core, insurance is protection from financial harm should particular events occur.

It may seem rudimentary at this stage to define something that we all know and use regularly. But when it comes to insurance, part of the problem is that we lose sight of its primary purpose.

We have countless options for when, where, and how to buy insurance for seemingly anything under the sun. In that environment, it can be challenging to make sense of things. Decision fatigue can shift insurance from a financial tool for a specific need to a nebulous salve for the general anxiety of “what if something goes wrong?”

There’s always a right tool for the job, and there’s also a right job for the tool.

While under-insuring yourself for critical costs can be disastrous, over-insuring can also sap your wealth over time. The only difference is that when you’re over-insured, it’s more of a death by a thousand cuts.

To avoid the pernicious impact of spending too much money on insurance, we need to understand the right time and technique to use self-insurance as an alternative.

How Does Self-Insurance Work?

Self-insurance is a practice whereby you take on the full responsibility of covering a particular risk rather than paying an insurance carrier.

Instead of an insurance company assuming some of the risk for you and charging a premium, you accept the entire risk (and responsibility for associated costs) yourself. Of course, you’re still welcome to charge yourself a premium if you want, but I wouldn’t recommend it.

In practice, self-insurance is simpler than it sounds. In most cases, it just means having enough savings available to cover potential costs.

For instance, imagine a retail store offers you an insurance plan for a new laptop, and you choose to self-insure instead. You would save the money that would have gone to the insurance plan premium, but the full responsibility of paying to repair or replace the laptop will fall to you if the need arises.

To properly self-insure in this scenario, you would need to make sure you have enough money available for that replacement. Whether that money falls under the umbrella of your regular emergency fund or goes into a dedicated savings account for self-insurance is up to you.

Self-Insured Vs. Uninsured

Is being self-insured the same as being uninsured? Not exactly, although the two may appear similar.

Both approaches cost nothing upfront and remain free as long as nothing goes wrong. Neither involves a written contract or signing up for private insurance.

However, choosing to be self-insured means taking ownership of your risk management, and in contrast, being uninsured means having no risk management.

The crucial difference is that a self-insured person understands and accepts the risk they are undertaking and has a plan should the worst happen. On the other hand, someone who doesn’t think about how to insure something at all relies entirely on hope.

Hope is beautiful, but it isn’t particularly useful in financial planning. Whether you are enlisting the services of an insurance company or managing things yourself, it’s always preferable to have a plan for financial risks.

Benefits of Self-Insurance

There are a few important reasons to consider self-insurance.

First, it is likely to save you money. Traditional insurance exists to make a profit when clients do not need (or are not eligible for) its reimbursement and support. Therefore, skipping insurance you don’t need will likely save you money.

Self-insurance also gives you freedom and flexibility. When you are your own insurer, you never have to file a compensation claim or worry about approval or whether you’re in compliance with your insurance policy. The policy is you, and you can always approve expenses for your number-one customer.

While it may be challenging to put a dollar value on simplicity and peace of mind, the value is undeniably there.

A self-insurance plan gives you one less bill to pay, one less bureaucratic maze to navigate, and one less series of looping automated phone calls to fight through. It means knowing that even if the worst happens, you have a plan, and you’re going to be okay, with no one standing in the way or waiting to fight you on it.

When Does It Make Sense to Self-Insure?

There are times when self-insurance can be a great way to save money and simplify your life, and times when the risk to your financial safety and health is far too high.

For instance, everyone should have a traditional auto insurance plan (particularly for liability in the case of accidents). When you are liable for injuries to another person, the legal and medical bills can be astronomical and more than most people can reasonably self-insure.

On the other hand, no one needs insurance for their new toaster because toasters are cheap and low-risk. So even in the worst case, you can buy a whole new toaster out of pocket.

But for everything in between, including the countless offers we receive for various insurance plans, how do we decide the right call? For instance, is cell phone insurance a scam or a prudent decision? Should you insure your new engagement ring or take the risk? What about travel insurance?

Let’s take a look at how we might approach questions like these.

Play It Safe or Roll the Dice?

When deciding whether or not to self-insure, there are two factors to consider:

- The likelihood of the risk

- The severity of the risk

How likely are you to incur costs, and how bad could they be?

If a particular scenario would likely bankrupt you (extreme severity), even if it’s relatively unlikely (low likelihood), you probably want coverage for it.

On the other hand, if the worst-case costs would be something you could manage (low-moderate severity), a traditional insurance plan is probably an unnecessary drain on your budget.

Of course, there are exceptions to both of these guidelines.

For instance, a volcanic eruption in your area would be a high severity event. Still, unless you live near an active volcano, the likelihood is low enough that it’s probably worth taking the risk.

Also, consider the case of insuring an appliance or electronic device. Compared to other things you might insure, losing or breaking a phone is a reasonably low severity outcome. For most people, self-insurance is fine here. However, suppose you are particularly clumsy or have a history of bad things happening to your devices. In that case, the high likelihood of it happening again might make the store insurance plan a good deal for you.

Self-insurance decisions always come down to whether the combined likelihood and severity of a risk makes it one you want to take yourself.

Making the Right Insurance Decisions for You

Every household will have its own unique needs and preferences for insurance, and there’s no one right way to do it. As the saying goes, personal finance is 80% personal and 20% finance.

You likely already have a sense of which types of insurance you definitely need and which ones you probably don’t. For everything else in between, consider the framework above to decide if self-insurance might be the easier, simpler, and more cost-effective option.

“Hope is beautiful, but it isn’t particularly useful in financial planning.” … Love this, and so true!!

Thanks! I’m all for optimism, but in an upcoming post we’re looking at the difference between hoping things will go well in the future and expecting they will.

Love this post. I’m almost entirely self insured (aside from liability, legal requirement, & homeowners). I’d be curious to know what you think about life insurance as an investment vehicle. I’ve been seeing a lot about this lately.

Thank you. Life insurance as an investment is a great example of why so much of this post emphasizes remembering what insurance is actually for: protecting from financial harm. In the case of life insurance, its purpose is to protect loved ones who rely on your income in the case you were no longer around to provide it. Pitching insurance as an investment vehicle distracts from that core purpose and convinces people to buy policies that they might not need otherwise. We don’t need our insurance to make us money, because that’s not its job. We’re generally better off investing in more conventional streams, like retirement accounts.